Sopact is a technology based social enterprise committed to helping organizations measure impact by directly involving their stakeholders.

Useful links

Copyright 2015-2025 © sopact. All rights reserved.

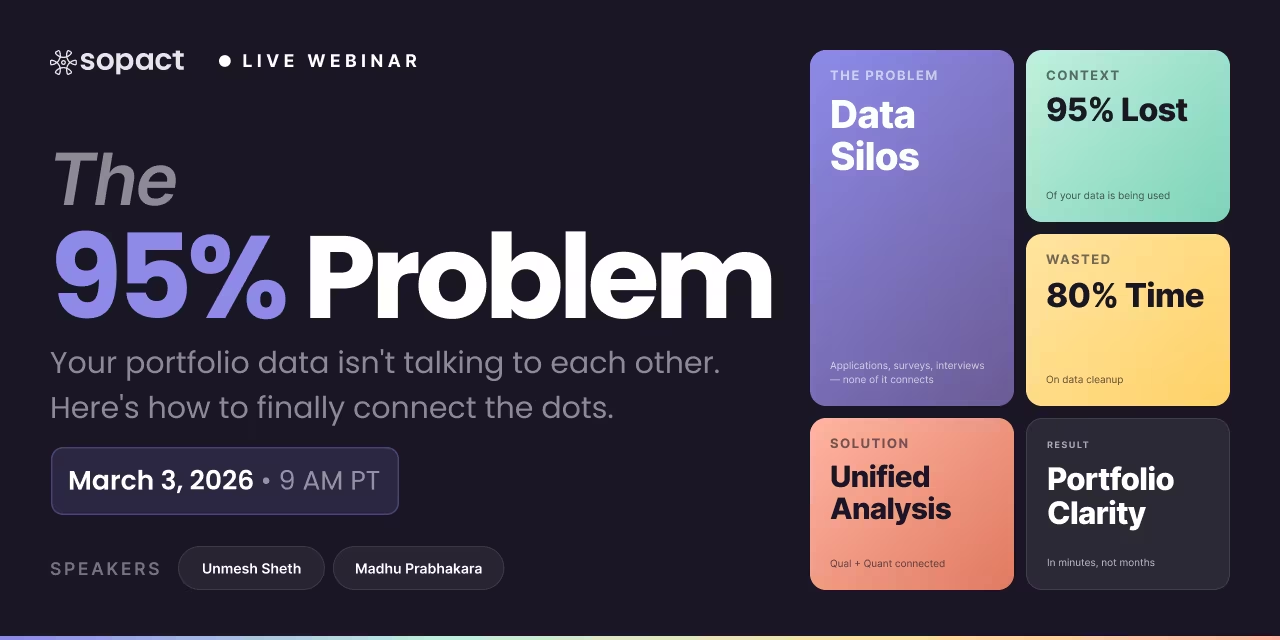

New webinar on 3rd March 2026 | 9:00 am PT

In this webinar, discover how Sopact Sense revolutionizes data collection and analysis.

ESG due diligence checklist: 24-point framework across E, S, and G pillars. AI scoring and persistent entity tracking for impact funds and supply chains.

Your investment committee meets in two hours. Three deals are on the table. Someone asks, "What's the ESG risk profile on these?" You have provider scores. You don't have understanding. The scores disagree with each other by 30 points, they were generated eight months ago from a static questionnaire, and none of them reflect what portfolio company stakeholders actually reported last quarter. That is The Scoring Trap — what happens when ESG due diligence optimizes for producing an auditable number instead of building actual understanding that holds up across a 3–5 year investment horizon.

Last updated: April 2026

The Scoring Trap is not a rating-agency problem. It is a structural gap in how ESG data is collected, linked, and analyzed across the full investment lifecycle — from pre-commitment due diligence through quarterly portfolio monitoring to LP reporting and CSDDD effectiveness documentation. This guide shows how Sopact Sense runs ESG due diligence as continuous intelligence rather than a frozen snapshot: structured DDQ collection at intake, AI reading every uploaded sustainability document with citation evidence, persistent portfolio company IDs connecting commitment to outcome, and longitudinal evidence chains that satisfy both LP reporting and regulatory effectiveness standards.

ESG due diligence is the structured evaluation of a company's environmental, social, and governance performance before an investment, acquisition, grant, or supplier relationship — and the continuous verification of that performance after the relationship begins. It covers three pillars — environmental impact and climate risk, social and labor practices, and governance quality — assessed through a combination of structured DDQs, document review, stakeholder feedback, and longitudinal monitoring. AI-native ESG due diligence reads every uploaded document end-to-end against anchored rubric criteria, producing citation-level evidence rather than provider-dependent scores that vary up to 50% for the same entity.

For impact funds, ESG due diligence sits alongside impact thesis validation — a social or environmental outcome theory must be evidenced as clearly as financial projections. For ESG-integrated private equity and sustainable investors, ESG DD is a pre-commitment risk screen that must hold up against CSDDD, SFDR, and LP reporting requirements throughout the holding period. For supply chain teams, ESG due diligence applies continuously across supplier networks with gender-disaggregated, region-specific data structures.

An ESG due diligence checklist is a structured data collection instrument covering the environmental, social, and governance dimensions that must be verified before a commitment and re-verified throughout the investment or vendor relationship. A functional ESG DD checklist is not a static 24-point PDF — it is a living rubric with observable evidence anchors at every scoring level, integrated into the DDQ and re-run against actual performance at each monitoring cycle.

Standard ESG DD checklist pillars include environmental (climate risk exposure, emissions disclosure, resource use, biodiversity, environmental management systems), social (workforce practices, health and safety, human rights, community engagement, supply chain labor standards), and governance (board independence, audit quality, whistleblower mechanisms, anti-bribery policies, ESG oversight accountability). Each pillar needs anchored scoring criteria specifying what observable evidence qualifies for each rating, not adjectives like "adequate" or "strong." Real-estate-focused ESG due diligence adds environmental liability, contamination history, and building energy performance. Supply chain ESG DD adds gender-disaggregated labor data, forced labor verification, and supplier tier mapping.

An ESG DDQ (Due Diligence Questionnaire) is the structured instrument an investor, funder, or procurement team sends to a prospective investee or supplier to collect standardized ESG data. It typically covers 40–150 questions across the three pillars, combining closed-ended compliance checks (certifications, policies, incident counts) with open-ended narrative responses (theory of change, corrective action plans, stakeholder engagement detail). A well-designed DDQ is evidence-anchored — every question maps to a rubric dimension, every open-ended response has AI coding instructions, and every financial field has validation rules at input.

An ESG score is what a rating provider (MSCI, Sustainalytics, ISS) produces from publicly available data. An ESG DDQ is what you collect directly from the entity being assessed. Scores vary up to 50% across providers for the same company. DDQs — when structured for AI analysis from the moment of submission — produce citation-linked evidence that holds up across regulatory review and LP diligence.

The Scoring Trap is the failure mode where ESG due diligence optimizes for producing an auditable number instead of building real understanding. Scores are provider-dependent, point-in-time, and non-reproducible — the same company scores 47 with one provider and 74 with another. For early-stage screening, a score is a reasonable anchor. But as your relationship with an investee, supplier, or grantee deepens, scores become actively misleading because they flatten the context that actually drives risk and opportunity.

Three structural failures define The Scoring Trap. First, scores are frozen. They capture one moment and are re-pulled annually or at exit, missing 11 months of context change per cycle. Second, scores reflect self-reported compliance, not stakeholder reality. A governance score can remain flat for three quarters while a critical labor risk emerges in worker-voice data that nobody reads. Third, scores cannot prove effectiveness. Under CSDDD, regulators require evidence that your ESG due diligence is actually "effective at preventing harm" — a single point-in-time score cannot demonstrate that. Only longitudinal evidence connected to the same entities across time can.

The progression Sopact Sense enables: SROI-style scoring as the entry point, contextual intelligence — theory of change data, qualitative stakeholder feedback, financial document analysis, persistent entity IDs — as the destination. Escaping The Scoring Trap means designing ESG data collection inside a single system from first contact, so qualitative and quantitative data link to the same entity record from day one.

ESG due diligence means different things to an impact fund manager screening 40 portfolio companies, a development finance institution evaluating gender-smart investments across Sub-Saharan Africa, and a procurement team verifying 200 supplier compliance records for CSDDD. The data you need, the timeline, and the depth of analysis differ fundamentally. Before building any framework, identify which situation you are in — then design your data collection accordingly. The three archetypes in the scenario below cover the patterns that appear in 90% of ESG DD engagements.

The highest-leverage action in ESG due diligence happens before any questionnaire is sent — designing a rubric with observable evidence anchors at every scoring level. An unanchored rubric criterion like "strong governance" means different things to every reviewer. Without calibration, DDQ completion rates look high while rubric interpretation fragments privately across your analyst team.

Anchored rubric criteria specify what evidence qualifies for each scoring level. A governance 5 might require a board with ≥40% independent directors, a documented whistleblower mechanism with reporting data, and an ESG oversight committee with defined charter. A governance 3 might describe the board qualitatively without documenting independence percentages. These anchors are what allow AI to score consistently across 40 portfolio companies or 200 suppliers and what allow human reviewers to calibrate against the same standard. Sopact Sense translates your existing DDQ — in any format, PDF, spreadsheet, or document — into AI-ready anchors while preserving your specific rubric dimensions and weights.

DDQ design for impact funds should integrate theory of change extraction alongside ESG scoring. Development finance DD needs gender-disaggregated fields structured at collection, not retrofitted from exports. Supply chain DD needs worker-voice survey instruments that code open-ended feedback for themes like forced overtime, retaliation, and wage issues. In every case, the DDQ is not a questionnaire — it is a data collection architecture that determines what kind of intelligence you can produce for the next five years.

AI-native ESG due diligence reads every submitted document — DDQ responses, sustainability reports, policy PDFs, incident logs, certifications, financial statements — against rubric criteria in parallel. The output is not a score. It is a scored dataset showing composite ratings, per-pillar breakdowns, and the specific content in each document that generated each rating, with citations back to source paragraphs.

For impact fund DD on 40 portfolio companies, AI processes every investment memo, onboarding transcript, and supplementary document — extracting logic model structure, populating financial metrics, and flagging ESG risk exposures — in the time it takes to make coffee. For development finance DD on 200 SME applications, AI scores every submission against the gender-smart rubric before a human reviewer opens a file; the review panel gets 40 ranked finalists with citation evidence rather than 200 raw applications. For supply chain DD across 150 suppliers, AI thematic analysis of open-ended worker feedback surfaces emerging risks by region within hours of survey close.

Citation evidence is non-negotiable. Every score must trace to the specific content that generated it. This is what satisfies CSDDD effectiveness requirements, what holds up under LP diligence, and what makes rubric iteration possible — because when you adjust a criterion, you can see exactly which entities' scores shift and why. See how this works across impact measurement and management, application review, and impact reporting.

The moment an investment closes or a supplier is onboarded, ESG due diligence should not end. It should continue as monitoring against the commitments captured at intake. Most ESG DD platforms fail at this transition — the DDQ data lives in one tool, quarterly reports arrive as PDFs in email, audit findings live in a third system, and worker-voice surveys live in a fourth. Without persistent entity IDs linking every instrument to the same company, monitoring becomes archaeological: compiled manually from disconnected sources, months after the decision window closes.

Sopact Sense assigns a persistent ID to every portfolio company, investee, or supplier at the point of first contact. Every subsequent data instrument — quarterly updates, financial document submissions, worker surveys, corrective action tracking, exit reports — connects to that same ID automatically. When your investment committee asks, "How has the governance score on Company X moved since intake?", the answer is one query, not three weeks of manual reconciliation. When CSDDD regulators ask you to prove your ESG DD is effective, the evidence chain is already assembled — intake commitment to mid-cycle verification to outcome measurement, all on the same entity record.

This is the difference between ESG due diligence as an event and ESG due diligence as a state. Event-based DD produces a filing cabinet. State-based DD produces intelligence. Learn more about continuous portfolio intelligence and how it unifies DD, monitoring, and LP reporting into a single evidence layer.

Under the EU Corporate Sustainability Due Diligence Directive (CSDDD), regulators require evidence that your ESG due diligence is "effective at preventing harm" — not just that it was performed. This is a fundamental shift from compliance-as-filing to compliance-as-proof. A point-in-time score cannot satisfy this. Only longitudinal evidence linking commitments at intake to verified outcomes across multiple reporting cycles can.

Sopact Sense generates CSDDD-ready evidence chains by default. Every entity has a persistent ID. Every DDQ submission is scored with citation evidence. Every corrective action is linked to the entity record. Every follow-up assessment is automatically compared to the prior cycle on the same entity. When regulators, auditors, or LPs ask for proof that your ESG DD is working, the chain is already assembled — intake commitment → mid-cycle evidence → corrective action → re-verification → outcome. This is what LPs increasingly expect from 2026 onward, and what competitors using provider-score aggregation cannot produce.

Mistake 1: Treating provider scores as the deliverable. Scores are a starting anchor, not a destination. Provider variance of 30–50 points for the same entity makes them unreliable as standalone decision tools. Move to contextual intelligence as data relationships deepen.

Mistake 2: Using the same DDQ for every deal type. A gender-lens facility in Sub-Saharan Africa needs different anchor criteria than a mid-market PE ESG screen in North America. Configure rubric dimensions per fund or per track.

Mistake 3: Importing from six tools instead of designing clean collection. Retrofitting analysis on top of messy data from Qualtrics, SurveyMonkey, and spreadsheets consumes 80% of assessment time. Start clean with data collection designed for AI analysis at the source.

Mistake 4: Static DDQ, no follow-up instruments. A DDQ filled at intake and never re-verified becomes an archaeological artifact by Year 2. Build follow-up instrument timing into the setup so persistent ID linkage is configured from day one.

Mistake 5: No thematic analysis of open-ended responses. Narrative DDQ fields contain the most valuable signal — and the least likely to be read at volume. AI thematic coding surfaces patterns across the full applicant or supplier pool that no manual reader could assemble.

Mistake 6: Treating ESG DD as separate from impact measurement. For impact funds especially, ESG DD and impact measurement and management must share the same entity records and the same data infrastructure. When they live in separate systems, neither produces defensible intelligence.

ESG due diligence is the structured evaluation of a company's environmental, social, and governance performance before an investment, acquisition, grant, or supplier relationship — and the continuous verification of that performance afterward. It covers three pillars (environmental, social, governance) assessed through structured DDQs, document review, stakeholder feedback, and longitudinal monitoring. AI-native ESG due diligence reads every uploaded document end-to-end against anchored rubric criteria, producing citation-level evidence rather than provider-dependent scores that vary up to 50% for the same entity.

An ESG due diligence checklist is a structured data collection instrument covering environmental, social, and governance dimensions that must be verified before a commitment and re-verified throughout the investment or vendor relationship. A functional ESG DD checklist is not a static PDF — it is a living rubric with observable evidence anchors at every scoring level, integrated into the DDQ and re-run at each monitoring cycle. Standard pillars include climate risk and environmental management, workforce and human rights, and governance quality.

An ESG DDQ (Due Diligence Questionnaire) is the structured instrument an investor, funder, or procurement team sends to a prospective investee or supplier to collect standardized ESG data. It typically covers 40–150 questions combining closed-ended compliance checks with open-ended narrative responses. A well-designed ESG DDQ is evidence-anchored — every question maps to a rubric dimension, every open-ended response has AI coding instructions, and every field has validation rules at input.

The Scoring Trap is the failure mode where ESG due diligence optimizes for producing an auditable number instead of building real understanding. Scores are provider-dependent (varying up to 50% for the same entity), point-in-time (captured once and re-pulled annually), and non-reproducible (reflecting self-reported compliance rather than stakeholder reality). Scores cannot satisfy CSDDD's requirement to prove effectiveness over time — only longitudinal evidence connected to the same entities across cycles can. Escaping The Scoring Trap means designing ESG data collection inside a single system from first contact.

An ESG due diligence framework is the methodology guiding how an organization collects, scores, and monitors ESG data across the investment or supplier lifecycle. Common frameworks include SFDR (Sustainable Finance Disclosure Regulation) for EU investors, CSDDD (Corporate Sustainability Due Diligence Directive) for large companies operating in the EU, IFC Performance Standards for development finance, and the ILPA ESG DDQ for institutional LPs evaluating fund managers. A good framework defines rubric dimensions, scoring weights, reporting cadence, and effectiveness evidence requirements — all configured in the data collection instrument at design time.

An ESG due diligence platform is the software system that hosts the DDQ, runs AI scoring against the rubric, manages entity records with persistent IDs, and generates reports for investment committees, LPs, or regulators. AI-native platforms read every uploaded document with citation evidence and connect DD data to continuous portfolio monitoring. Sopact Sense is an AI-native ESG DD platform purpose-built for impact funds, development finance institutions, and sustainability-led investors — combining DDQ design, rubric scoring, longitudinal monitoring, and CSDDD evidence chains in a single platform.

Environmental due diligence is the subset of ESG due diligence focused on environmental risk exposure — climate risk, emissions, resource use, biodiversity, contamination history, and environmental management systems. For real estate transactions, environmental due diligence additionally covers site contamination, remediation liability, building energy performance, and regulatory compliance at the asset level. For investment DD, environmental due diligence assesses the company's climate alignment, transition plan, and physical-risk exposure. The data structures differ between asset-level and entity-level environmental DD — both require anchored scoring criteria and ongoing monitoring, not one-time assessment.

Gender-smart ESG due diligence integrates gender-disaggregated data collection and gender-lens scoring criteria into the DDQ at the point of submission. Standard dimensions include women in leadership percentages (typical target 40%), gender of primary beneficiaries, gender pay equity indicators, and theory of change for gender outcomes. Development finance institutions and gender-lens funds require gender-smart DD because funder requirements increasingly mandate gender-disaggregated evidence. The key architectural decision is structuring gender fields at collection, not retrofitting from a spreadsheet export after submission.

CSDDD is the EU Corporate Sustainability Due Diligence Directive, which requires large companies operating in the EU to identify, prevent, and remediate adverse human rights and environmental impacts across their value chains. The directive requires evidence that due diligence is "effective at preventing harm" — not just that DD was performed. This is a fundamental shift: a point-in-time score cannot satisfy this standard. Only longitudinal evidence linking commitments at intake to verified outcomes across multiple reporting cycles can. ESG DD platforms must generate CSDDD-ready evidence chains by default, with persistent entity IDs connecting intake to effectiveness proof.

The best ESG DD platform for impact funds depends on portfolio size, LP reporting requirements, and whether ESG DD is integrated with impact measurement or run separately. For impact funds with 10+ portfolio companies that need AI-extracted logic models, persistent entity IDs, and integrated impact measurement alongside ESG scoring, Sopact Sense is purpose-built for the continuous intelligence model. Provider score aggregators (MSCI, Sustainalytics) serve a different need — early-stage screening based on public data. The two are complementary; Sopact Sense handles the DD engagement and longitudinal monitoring; provider scores can feed in as one input signal.

ESG due diligence software pricing varies widely by scope. Provider score subscriptions (MSCI, ISS, Sustainalytics) typically run $15,000–$75,000 per year depending on coverage. Traditional DDQ platforms (for private markets DD) run $20,000–$100,000+ per year. AI-native platforms like Sopact Sense scale with portfolio size and use-case complexity. Request a walkthrough for pricing specific to your portfolio size, LP reporting requirements, and integration needs.

Supply chain ESG due diligence applies the ESG DD rubric across supplier networks with two architectural additions: persistent supplier IDs connecting DDQ submissions to worker-voice surveys to corrective action tracking, and AI thematic analysis of open-ended worker feedback at scale. For CSDDD compliance, the supplier DDQ must generate evidence that due diligence is effective at preventing harm — which requires longitudinal data on the same supplier entities, not isolated snapshots. Tools that simplify ESG due diligence for supplier networks must handle both the structured rubric scoring and the unstructured worker-voice analysis within a single connected system.