ESG Due Diligence: Checklist, Framework & AI Platform

ESG due diligence checklist: 24-point framework across E, S, and G pillars. AI scoring and persistent entity tracking for impact funds and supply chains.

Founder & CEO of Sopact with 35 years of experience in data systems and AI

ESG Due Diligence: Checklist, Framework, and AI-Native Platform

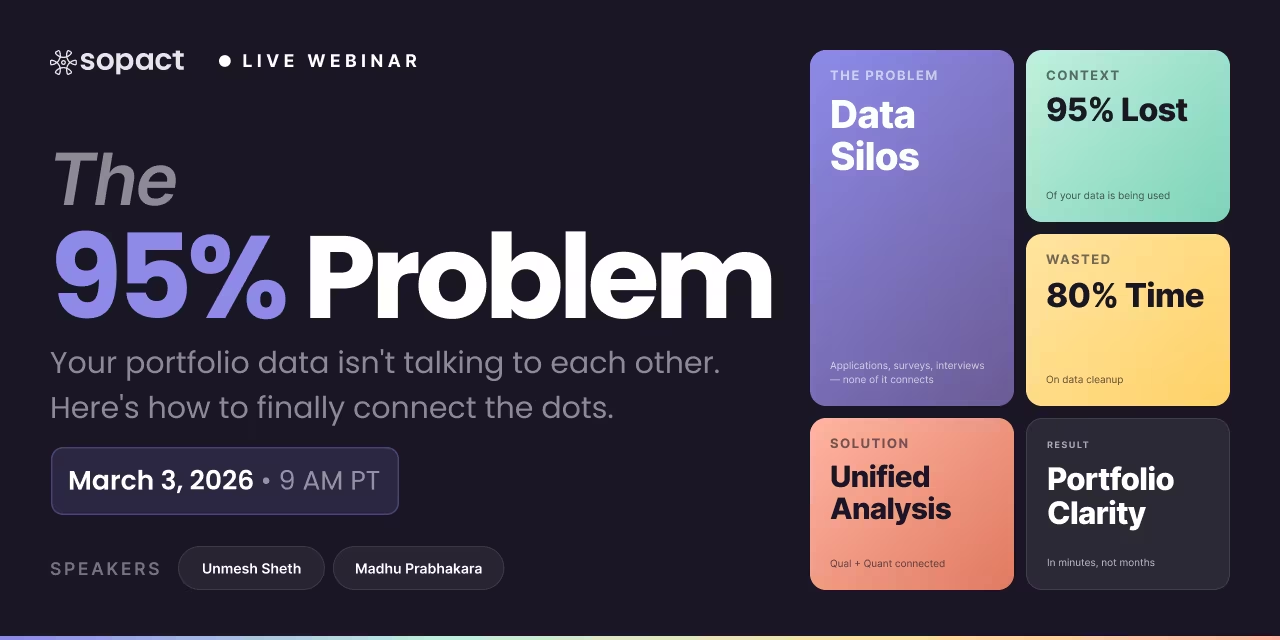

Your investment committee meets in two hours. Three deals are on the table. Someone asks: "What's the ESG risk profile on these?" You have provider scores. You don't have understanding. The scores disagree with each other by 30 points, they were generated eight months ago from a static questionnaire, and none of them reflect what portfolio company stakeholders actually reported last quarter. That's not a data problem. That's The Scoring Trap.

The Scoring Trap is what happens when ESG due diligence optimizes for producing an auditable number instead of building actual understanding. Scores are provider-dependent, point-in-time, and non-reproducible — the same company scores 47 with one provider and 74 with another. For early-stage screening, a score is a reasonable starting point. But as your relationship with an investee, supplier, or grantee deepens, scores become actively misleading because they flatten the context that drives real decision-making.

This guide shows how Sopact Sense supports ESG due diligence across three modes — impact fund portfolio assessment, development finance deal screening, and supply chain compliance — using a progression that starts with structured scoring and matures into contextual intelligence as your data relationship deepens.

New Framework

The Scoring Trap

ESG due diligence that produces an auditable score is useful as a starting point. Scores become a liability when they substitute for understanding — varying up to 50% across providers for the same entity, reflecting self-reported compliance rather than stakeholder reality, and unable to satisfy CSDDD's requirement to prove effectiveness over time. Sopact Sense enables the progression: SROI-style scoring as the entry point → contextual intelligence as the destination.

50%

ESG score variance for the same entity across providers

80%

Of ESG assessment time spent cleaning data, not analyzing it

5%

Of portfolio insights actually captured using manual CRM-based workflows

ESG due diligence means different things to an impact fund manager screening 40 portfolio companies, a development finance institution evaluating gender-smart investments, and a procurement team verifying 200 supplier compliance records. The data you need, the timeline, and the depth of analysis differ fundamentally across these contexts. Before building any framework, identify which situation you're in — then design your data collection accordingly.

Define Your ESG Due Diligence Situation

Three modes — each with different data needs, timelines, and depth requirements

① Describe your situation

② What to bring

③ What Sopact Sense produces

Impact Fund

Portfolio is expanding faster than the team can onboard and track companies

"I'm the portfolio operations lead at an impact fund. We have 19 companies now, expanding to 40+ by June. Every time we onboard a new company, my analyst spends 2–3 hours manually pulling theory of change and logic model data from investment memos and call notes. Our CRM tracks deals but has zero impact context. Financial documents are parsed by hand. When we collect quarterly data, companies submit in completely different formats — we spend 80% of our time cleaning instead of analyzing. I need to solve this before we hit 40 companies."

Platform signal: Sopact Sense is the right tool when you have 10+ portfolio companies and need AI-extracted logic models, persistent company IDs, financial document parsing, and quarterly monitoring without adding headcount. For 1–5 companies tracked informally, a structured spreadsheet template may serve you until the portfolio grows.

Development Finance

Deal applications need gender-smart scoring, but investee data arrives inconsistently across geographies

Program officers · Gender-lens investors · DFI analysts · Foundation program staff

›

"I'm a program officer at a development finance institution. We receive 200+ deal applications from SMEs across Sub-Saharan Africa. Our funder requires gender-smart due diligence — women in leadership percentages, gender-disaggregated beneficiary data, theory of change for gender outcomes. Every applicant submits in a different format. Some send PDFs, some send email attachments, some fill out a Google form. We have no consistent way to score qualitative gender criteria alongside quantitative financial metrics, and no system that connects initial screening data to how these investees perform over a 3–5 year investment period."

Platform signal: Sopact Sense designs the application intake form with gender-smart criteria structured at collection — not retrofitted from exports. Qualitative and quantitative fields are in the same instrument, AI-scored against your rubric, with persistent investee IDs connecting screening data to 5-year monitoring cycles.

Supply Chain Compliance

Supplier assessments produce scores, but corrective actions can't be connected to follow-up evidence

"I manage ESG compliance for 150 suppliers across three regions. We collect worker voice surveys in one tool, audit findings come in as PDFs, corrective action plans live in spreadsheets, and financial compliance data is in a separate system. When I need to show the board that our due diligence is actually reducing labor risks — not just producing scores — I can't connect the Q1 worker survey data to the Q3 re-survey because they're in different systems with no shared entity ID. CSDDD compliance requires we prove effectiveness over time and I don't have the architecture to do that."

Platform signal: Sopact Sense is the right tool when you need persistent supplier IDs connecting DDQ → corrective action → re-survey across all cycles, and AI thematic analysis of open-ended worker feedback across 100+ supplier sites simultaneously. For a one-time static checklist on 5 suppliers, a structured Excel template is sufficient.

📋

Assessment Rubric or Criteria

Define your scoring dimensions before collection begins — theory of change clarity, gender-smart criteria, labor standards, governance quality. Weight each dimension explicitly.

📝

DDQ or Application Form Design

Map each intake question to its rubric dimension. Open-ended questions need AI coding instructions. Financial fields need validation rules at input.

👥

Stakeholder Roles

Who submits initial data (investee, supplier, grantee), who reviews (analyst, program officer), who approves (investment committee, board). Configure role-based access before launch.

📅

Assessment Timeline and Cycles

Pre-investment screening timeline, quarterly monitoring cadence, annual audit cycle. Define follow-up instrument timing so persistent ID linkage is configured at setup.

📊

Prior Cycle Data

If this is not the first assessment cycle, bring prior cycle data structured by entity. Sopact Sense assigns persistent IDs at first contact — prior unstructured data should be imported with entity mapping at setup.

📄

Financial Documents and Memos

For impact fund and development finance modes: investment memos, financial statements, and onboarding transcripts for AI logic model extraction and financial metric population.

Edge case note: For multi-funder portfolios where each funder requires different rubric dimensions, configure Sopact Sense with a core shared rubric plus funder-specific field extensions. Do not create separate collection instruments per funder — this breaks the persistent entity ID connection across your combined portfolio.

From Sopact Sense — ESG Due Diligence Outputs

Logic model extraction: Theory of change frameworks pulled from investment memos and onboarding transcripts automatically — not assembled manually per company

DDQ scoring with AI analysis: Every submission scored against your rubric the moment it arrives; open-ended qualitative responses coded for themes across the full applicant or supplier pool

Financial document parsing: Key metrics extracted from uploaded statements and populated into entity records without manual data entry

Persistent entity scorecard: Each portfolio company, investee, or supplier has a connected longitudinal record — every assessment cycle is compared automatically, not rebuilt from scratch

Portfolio-level intelligence: Thematic patterns across all entities flagged; entities below threshold criteria surfaced for review; trend lines across reporting cycles available without custom export work

CSDDD effectiveness chain: Corrective actions linked to entity records; follow-up assessment data automatically compared to prior cycle on the same entity; evidence trail ready for regulatory documentation

Next prompt — Impact Fund

"We're onboarding 6 new portfolio companies next month. Build the intake DDQ with theory of change extraction, financial metrics, and governance scoring — all connected to the same unique company ID from first submission."

Next prompt — Development Finance

"We have 200 applications coming in. Score each against our gender-smart rubric and flag the top 40 by composite score. Show me which applicants in positions 41–60 would move up if we weighted gender-leadership criteria at 35%."

Next prompt — Supply Chain

"Q1 worker surveys are complete across 150 suppliers. Show me the theme frequency for labor rights issues by region. Flag any supplier where 'forced overtime' or 'retaliation' appeared in more than 15% of open-ended responses."

The Scoring Trap: Why ESG Scores Fail as Your Only Tool

ESG scores solve a real problem at the start of a due diligence relationship: they provide a comparable, structured baseline when you have limited time and limited context. An SROI calculation, a supplier risk score, or a third-party ESG rating gives you a defensible anchor for early-stage screening. That's appropriate and correct.

The problem starts when scores become the destination rather than the entry point. Third-party ESG scores for the same entity can vary by up to 50% across rating providers. Scores reflect what organizations self-report, not what workers or beneficiaries experience. A governance score can remain flat for three consecutive quarters while a critical labor risk is emerging in qualitative feedback that nobody read. And under CSDDD, a score cannot prove your due diligence is "effective at preventing harm" — only longitudinal evidence connected to the same entities across time can satisfy that standard.

The progression Sopact Sense enables: SROI-style scoring gets you started. Contextual intelligence — theory of change data, qualitative stakeholder feedback, financial document analysis, and longitudinal tracking linked by persistent entity IDs — is where you arrive as relationships deepen. The Scoring Trap is choosing not to make that transition.

Organizations that escape the Scoring Trap share one architectural decision: they design data collection inside a single system from first contact, so qualitative and quantitative data are linked to the same entity record from day one. They don't import from six tools. They start clean, and they stay clean.

Step 2: How Sopact Sense Runs ESG Due Diligence Data Collection

Sopact Sense is a data collection platform — not a downstream aggregation layer. Every entity assessed (portfolio company, investee, supplier, grantee) receives a unique persistent ID at the point of first contact: the initial DDQ submission, deal application, or supplier onboarding intake. Every subsequent data instrument — progress surveys, financial questionnaires, follow-up assessments — connects to that same ID automatically. Unlike Qualtrics or SurveyMonkey, which collect data without analysis, Sopact Sense structures every field for AI analysis from the moment of submission.

For an impact fund, Sopact Sense designs the initial portfolio company DDQ inside the platform. AI extracts theory of change frameworks from uploaded investment memos and onboarding transcripts — populating logic model fields automatically rather than requiring 2–3 hours of manual assembly per company. Financial document analysis reads uploaded statements and populates key metrics into the portfolio record without manual extraction. When a portfolio expands from 20 to 40 companies, no additional analyst headcount is required to maintain data quality.

For a development finance institution running deal screening, Sopact Sense hosts the application intake form with gender-smart criteria structured at the point of collection — not retrofitted from a spreadsheet export. Disaggregation by gender, geography, and sector is built into the data model from the first submission. AI analyzes open-ended qualitative responses across the full applicant pool for thematic patterns before any human reviewer opens a file. This is the same architecture Sopact deploys for grant reporting and impact measurement and management.

For supply chain compliance, Sopact Sense designs and deploys the supplier self-assessment DDQ and worker voice surveys inside the same platform. Open-ended worker feedback is coded by AI for themes, sentiment, and emerging risks across all supplier sites simultaneously — the kind of analysis that is structurally impossible when worker surveys live in one tool and audit findings live in another. This aligns directly with what teams building program evaluation frameworks already know: clean-at-source collection eliminates the 80% data cleanup tax.

What Sopact Sense does not do: import scores from third-party rating providers, aggregate audit exports from external platforms, or serve as a reporting layer for data collected in separate systems. Sopact Sense is where ESG due diligence data collection starts. That architectural commitment — not adding AI to existing messy workflows, but designing clean collection from the beginning — is what makes downstream intelligence possible.

For Impact Funds

Your LP report is three weeks away — or overnight.

Sopact reads every investee document, holds every DD commitment, and generates all six LP-ready reports the night the quarter closes.

Step 3: The ESG Due Diligence Checklist — What Each Mode Requires

A functional ESG due diligence checklist is not a static 24-point PDF. It is a structured data collection instrument aligned to the specific assessment context, with qualitative and quantitative fields linked to the same entity record, built for AI analysis from the moment of submission. The three pillars — Environmental, Social, Governance — apply across all modes. The data fields, scoring weights, and follow-up instruments differ by who is being assessed and why.

The Phase-by-Phase workflow for each mode is shown below — covering setup, active assessment, and longitudinal monitoring.

ESG Due Diligence — Phase-by-Phase Workflow

Select your due diligence mode to see the full three-phase checklist and Sopact Sense output

Impact Fund Portfolio

Development Finance

Supply Chain Compliance

Phase 1

Setup — Build the Portfolio DDQ and Logic Model Extraction System

Portfolio Operations Lead — Setup Prompt

"I run portfolio operations at an impact fund. We're onboarding 8 new companies this quarter, reaching 27 total. Build a portfolio intake DDQ that covers theory of change, financial health indicators, governance quality, and ESG risk exposure across E, S, and G pillars. Each new company should receive a unique persistent ID from the moment they submit intake — connecting all future quarterly updates, financial documents, and survey responses to the same record. For each new company, automatically extract logic model structure from their uploaded investment memo."

Sopact Sense produces

Portfolio intake DDQ with five scored dimensions: theory of change clarity (25%), social impact potential (20%), ESG risk exposure (20%), financial health (20%), governance quality (15%) — each field mapped to its rubric dimension for AI pre-scoring

Unique company ID assigned at first submission — connecting intake DDQ, quarterly update surveys, financial documents, and governance assessments into a single longitudinal record for every company

AI logic model extraction from each uploaded investment memo: theory of change diagram, key outcome indicators, and target population data auto-populated into the portfolio record — eliminating the 2–3 hour manual assembly task per company

Financial metric extraction template: key metrics pulled from uploaded financial statements (revenue, burn rate, mission-critical ratios) and populated into the portfolio record without manual parsing

Portfolio overview dashboard: all 27 companies visible with intake scores by dimension, logic model completeness status, and outstanding submission flags — ready before any quarterly review

Phase 2

Assessment — Score the Portfolio and Generate Due Diligence Reports

Portfolio Operations Lead — Assessment Prompt

"All 8 new companies have completed intake. Generate the due diligence scorecard for our investment committee. Show me the composite ESG score for each company by pillar. Flag any company where governance scored below 1.5 out of 3 — that's a committee discussion threshold. Also show me which companies have a strong theory of change score but low financial health score — those need a different type of support conversation before we can report them to LPs."

Sopact Sense produces

Due diligence scorecard for all 8 new companies: composite ESG score + individual pillar scores (E, S, G), theory of change quality score, and financial health rating — all traced to specific intake responses

2 companies flagged with governance below 1.5 threshold — committee-ready flag with score rationale pulled from their open-ended governance disclosures, identifying board independence and whistleblower mechanism gaps

Quadrant analysis: 3 companies show strong theory of change (above 2.2) but low financial health (below 1.4) — identified as capacity-building candidates before LP reporting cycle

AI thematic analysis of open-ended ESG narrative responses across all 8 companies: identifies "data measurement capacity" as the most common gap theme in 5 of 8 new company responses — informs portfolio-level capacity support plan

Committee-ready export: PDF due diligence report per company, composite portfolio scorecard with flagged exceptions, and LP-format summary — all generated from the same data collection without additional formatting work

Phase 3

Monitoring — Quarterly Portfolio Updates and Longitudinal Comparison

Portfolio Operations Lead — Q3 Monitoring Prompt

"Q3 portfolio updates are complete. 24 of 27 companies submitted. Generate the Q3 portfolio scorecard and compare to Q2 on ESG pillar scores for each company. For the 3 companies that flagged governance concerns at intake — show me whether their Q3 governance scores improved. Also generate the LP impact report summarizing portfolio-level ESG trend data for the full 27-company portfolio."

Sopact Sense produces

Q3 portfolio scorecard: 24 companies with current ESG pillar scores compared against Q2 baselines — all pulled from the persistent ID-linked records, no manual reconciliation required

Governance trend for the 3 flagged companies: 2 improved (average governance score up from 1.3 to 1.8), 1 still below threshold (currently 1.4) — flagged for portfolio manager follow-up with corrective action recommendation

Portfolio-level ESG trend: Environmental scores improved across 18 of 24 companies (avg +0.3 points); Social scores flat (avg +0.05); Governance showing highest variance — identified as the portfolio's primary systematic risk area

3 pending companies noted with Q2 scores as estimated proxies — board briefed on projected complete figures and historical submission delay patterns

LP impact report: narrative portfolio summary, ESG trend charts, qualitative highlights from AI analysis of open-ended responses, and theory of change progress across the portfolio — formatted for LP submission without additional design work

Phase 1

Setup — Build the Gender-Smart Application Intake and Scoring Rubric

Program Officer — Setup Prompt

"I'm the program officer for a gender-lens investment facility. We receive 200+ SME applications from Sub-Saharan Africa each cycle. Our funder requires gender-smart due diligence: women in leadership (target 40%), gender-disaggregated beneficiary data, and a theory of change for gender outcomes. Build an application intake form with five scored dimensions: gender leadership representation (25%), gender-smart business model (25%), social and environmental ESG baseline (20%), financial readiness (20%), and theory of change quality (10%). All qualitative dimensions should be AI-scored before any human reviewer sees the application."

Sopact Sense produces

Gender-smart application intake form with five weighted rubric dimensions — each open-ended response field mapped to its dimension for AI pre-scoring before human review

Unique investee ID assigned at application submission — connecting this application to all future progress surveys, financial reports, and outcome assessments over the 3–5 year investment period

Gender-disaggregated data fields structured at collection: women in leadership %, gender of primary beneficiaries, gender pay equity indicator — not retrofitted from an export after submission

Reviewer interface: AI pre-score per dimension with rationale displayed alongside blank reviewer override field — calibrated starting point, not forced agreement, consistent across all 200+ applications

Threshold configuration: applications where women in leadership falls below 30% are flagged for committee discussion; applications with no gender-disaggregated beneficiary data are flagged as incomplete before entering the review queue

Phase 2

Screening — Score Applicants and Generate Deal Selection Scorecard

Program Officer — Screening Prompt

"Review is closed. 187 complete applications received. Generate the ranked deal selection scorecard for our investment committee. Show the top 30 by composite score. Flag any in the top 30 where the gender leadership dimension scored below 1.5 — that's a non-negotiable threshold for our funder. Also show me: if we increased gender-smart business model weighting to 35%, which applicants currently in positions 31–50 would move into the top 30?"

Sopact Sense produces

Ranked scorecard of all 187 applications by weighted composite score — filterable by country, sector, and business size

Top 30 highlighted with gender leadership scores displayed — 4 applications flagged with gender leadership dimension below 1.5 threshold, with AI rationale from their open-ended response on gender policies

Sensitivity analysis: 6 applications in positions 31–50 would enter the top 30 if gender-smart business model weighting increased to 35% — current composite and gender-smart scores shown for each

AI thematic analysis of top 30 applicants' theory of change narratives: identifies "informal market access" as the dominant gender outcome pathway (22 of 30 applicants) — informs portfolio strategy framing for funder reporting

Committee-ready export: PDF deal selection scorecard ranked by composite score, reviewer notes, AI rationale summaries, gender dimension highlights, and flagged threshold exceptions — formatted for on-screen committee presentation

Phase 3

Monitoring — Investee Progress Tracking Over the Investment Period

Program Officer — Year 2 Monitoring Prompt

"We've selected 22 investees. It's 18 months into the investment period. Generate the Year 1.5 portfolio monitoring report. Show me each investee's gender leadership percentage compared to their baseline at application — who has improved, who has declined. Also show how gender-disaggregated beneficiary data has shifted across the portfolio since deal close. Flag any investee where women in leadership has declined more than 5 percentage points from their application baseline."

Sopact Sense produces

18-month portfolio monitoring report: 22 investees with current gender leadership percentage vs. application baseline — pulled from persistent ID-linked records connecting application data to 18-month progress survey with no manual reconciliation

Gender leadership trend: 15 investees improved or held steady; 5 declined from baseline; 2 flagged with declines exceeding 5 percentage points — one now at 28% (was 38% at application), one at 31% (was 42%)

Gender-disaggregated beneficiary shift: portfolio-level women beneficiary percentage improved from 54% at baseline to 61% at 18 months — driven primarily by 6 investees in the informal retail sector

AI analysis of open-ended progress responses: "leadership pipeline gaps" identified as the dominant theme in 8 of 22 investee narratives — suggests a portfolio-wide capacity support intervention on women's leadership development

Funder progress report: narrative summary with gender outcome trend data, longitudinal charts comparing application baseline to 18-month results, qualitative highlights from AI analysis — formatted for Mastercard Foundation or equivalent funder submission

Phase 1

Setup — Build the Supplier DDQ and Worker Voice Survey System

ESG Compliance Lead — Setup Prompt

"I manage ESG compliance for 150 suppliers across Southeast Asia and East Africa. Build a supplier DDQ that covers Environmental (emissions reporting, water stewardship, waste), Social (labor practices, health and safety, worker voice), and Governance (anti-corruption, board oversight, whistleblower mechanisms) — each mapped to our CSDDD-aligned rubric. Alongside the DDQ, build a worker voice survey for each supplier site, linked to the same supplier ID, with open-ended questions about working conditions that Intelligent Cell can analyze for forced labor themes and retaliation risk."

Sopact Sense produces

Supplier DDQ with 18 scored criteria across E, S, and G pillars — each field mapped to its CSDDD-aligned rubric dimension for AI pre-scoring at submission; no manual scoring by analyst required

Unique supplier ID and unique factory-site ID assigned at first DDQ submission — connecting this assessment to all future corrective action records, follow-up DDQs, and worker voice surveys

Worker voice survey linked to same supplier ID: structured fields for health and safety incidents, plus open-ended questions ("Describe any pressures you feel at work that make it difficult to raise concerns") — mapped to forced labor and retaliation rubric for AI coding

AI thematic coding configured: forced labor, retaliation, excessive overtime, freedom of association, and wage withholding as primary theme categories — with frequency scoring across all supplier sites activated from first response wave

CSDDD compliance baseline: every submission timestamped and source-linked — building the audit trail that proves due diligence was conducted with specific entities, on specific dates, with corrective actions linkable from the same record

Phase 2

Assessment — Score Suppliers and Generate Compliance Report

ESG Compliance Lead — Q1 Assessment Prompt

"Q1 DDQs and worker voice surveys are complete across 142 of 150 suppliers. Generate the Q1 supplier compliance scorecard. Rank suppliers by composite ESG score. Flag any supplier where Social pillar scored below 1.5. Show me which suppliers had 'forced overtime' or 'retaliation' appear in more than 15% of their worker voice open-ended responses. I need to bring corrective action recommendations to the board next week."

Sopact Sense produces

Q1 compliance scorecard: 142 suppliers ranked by composite E, S, G score — filterable by country, product category, and tier (direct vs. indirect supplier)

11 suppliers flagged with Social pillar below 1.5 threshold — distributed across 3 countries; 7 are Tier 1 direct suppliers, 4 are Tier 2

Worker voice risk flags: 6 suppliers where "forced overtime" appeared in more than 15% of open-ended responses; 2 suppliers where "retaliation" appeared in more than 15% — all 8 cross-referenced against their DDQ Social scores to identify whether self-reported and worker-reported data are aligned or diverging

Divergence alert: 3 suppliers scored above 2.0 on their DDQ Social dimension but have worker voice flags above threshold — indicating self-reported compliance may not reflect actual worker experience; flagged for priority corrective action

Board corrective action brief: 8 priority suppliers identified with specific flags, corrective action recommendations per supplier (remediation plan template, third-party verification trigger, re-survey timeline), and CSDDD evidence trail documentation showing the full assessment chain

Phase 3

Monitoring — Corrective Action Tracking and CSDDD Effectiveness Proof

ESG Compliance Lead — Q3 Follow-Up Prompt

"It's Q3. All 8 suppliers flagged in Q1 completed corrective action plans. Q3 worker voice surveys are in for those same suppliers. Show me: did the forced overtime and retaliation theme frequencies drop at the flagged sites? Compare Q1 and Q3 theme frequency per supplier. This is the effectiveness evidence we need for our CSDDD submission."

Sopact Sense produces — CSDDD effectiveness chain

Q1 vs. Q3 theme frequency comparison for all 8 corrective action suppliers: data pulled from the same supplier IDs with no manual reconciliation — entity continuity guaranteed by persistent ID architecture

Forced overtime: frequency dropped from above 15% threshold in Q1 to below 8% in Q3 for 6 of 8 suppliers; 2 suppliers still above 10% — flagged for continued corrective action and potential third-party audit escalation

Retaliation: frequency dropped from above 15% to below 5% for both flagged suppliers — both corrective actions (anonymous reporting mechanism installation, manager retraining) documented as completed in the same supplier records

CSDDD effectiveness evidence package: timestamped Q1 assessment → corrective action plan (linked to supplier record) → Q3 re-assessment → theme frequency comparison — presented as a complete, auditable chain per supplier, formatted for regulatory submission

Board summary: total portfolio ESG improvement Q1 to Q3; 6 of 8 corrective actions achieving target; 2 requiring escalation; CSDDD effectiveness documentation complete for 6 suppliers, pending for 2 — with projected Q4 completion date

What the ESG Due Diligence Questionnaire Must Capture

The ESG DDQ is the primary intake instrument. Unlike a compliance checkbox form, a well-designed DDQ captures three data types simultaneously: structured quantitative fields (emissions figures, workforce demographics, board composition ratios), scored qualitative dimensions (theory of change clarity, community engagement depth, governance transparency), and open-ended narrative responses that require AI analysis at scale. Platforms like Qualtrics collect the first type. They do not score the second, and they do not analyze the third. Sopact Sense structures all three in the same instrument, linked to the same entity record, analyzed in the same platform — the same approach used in impact investment examples and social impact consulting workflows.

ESG Due Diligence Report: What Comes Out

The ESG due diligence report is the output that moves decision-making. A report generated from Sopact Sense data includes: entity score by pillar traced to specific instrument responses; AI thematic coding of qualitative narratives from open-ended fields with theme frequency across the portfolio; financial document key metrics automatically extracted and populated; flagged discrepancies between self-reported qualitative responses and quantitative data; and longitudinal comparison to the prior assessment cycle where the persistent ID enables direct entity-to-entity comparison. This is not a compliance dashboard. It is an intelligence output that explains why a score changed and whether prior corrective actions moved any metrics.

Step 4: Gen AI Tools vs. Sopact Sense for ESG Analysis

Impact funds, development finance teams, and procurement teams are increasingly using ChatGPT, Claude, and Gemini to analyze ESG data — uploading spreadsheets and PDF reports and asking AI to produce due diligence summaries. The outputs are useful for drafting. They are structurally unreliable for decision-making at portfolio scale.

Non-reproducible analytical results mean the same ESG analysis run Monday and Friday produces different thematic outputs, different risk flags, and different recommended actions. ESG due diligence requires consistent methodology across your portfolio. Non-deterministic AI analysis makes cross-entity comparison impossible — which is the core task.

No persistent entity tracking means every generic AI session starts from zero. The longitudinal context — what changed quarter over quarter, which corrective actions worked, which risks are trending upward across your supplier base — is completely invisible. The Scoring Trap gets worse, not better, when you add generic AI to static workflows.

Disaggregation inconsistencies mean that gender, geography, and sector breakdowns produce different segment labels across AI sessions. Equity analysis built on inconsistent disaggregation produces conclusions that cannot be compared quarter to quarter — a direct problem for gender-smart investment reporting and CSDDD effectiveness documentation.

Unstructured inputs corrupt structured outputs. When financial documents, worker surveys, and audit reports are uploaded as individual files to a generic AI session, there is no guarantee the AI is comparing equivalent data points across entities. Sopact Sense structures data at the point of collection so comparison across 40 portfolio companies or 200 suppliers is comparing identical fields.

1

Non-Reproducible Analysis

Run the same ESG prompt Monday and Friday — different thematic outputs, different risk flags, different entity rankings. Cross-portfolio comparison requires identical methodology. ChatGPT is non-deterministic by design.

2

No Persistent Entity Memory

Every generic AI session starts from zero. The longitudinal context — what changed quarter over quarter, which corrective actions worked, which labor risks are trending — is completely invisible to the model.

3

Disaggregation Inconsistencies

Gender, geography, and sector breakdowns produce different segment labels across AI sessions. Equity analysis built on inconsistent disaggregation cannot be compared quarter to quarter — a direct problem for CSDDD effectiveness documentation.

4

Unstructured Inputs, Unreliable Outputs

Uploading financial statements, worker surveys, and audit reports as individual files to a generic AI session means there is no guarantee the model compares equivalent data points across entities. Structural problems surface two cycles later.

← Scroll to see full comparison

Dimension

✕ Gen AI Tools (ChatGPT / Gemini / Claude)

✓ Sopact Sense

Entity Tracking

No persistent entity memory — each session starts from zero; longitudinal comparison requires manual file assembly every cycle

Persistent unique ID assigned at first submission; every subsequent assessment, corrective action, and re-survey connected automatically

Qualitative Analysis

Non-reproducible thematic outputs — same worker survey file produces different themes, different frequencies, different risk flags across sessions

Consistent AI coding against configured rubric categories (forced labor, retaliation, governance gaps) — theme frequencies comparable across cycles and entities

Disaggregation

Segment labels shift across sessions — gender, geography, and sector breakdowns are inconsistent; equity analysis is unreliable for regulatory reporting

Disaggregation structured at collection — gender, location, sector fields are standardized data model fields, not AI-inferred labels; fully consistent across all cycles

Logic Model Extraction

Can draft a theory of change from a memo — but output changes each run, is not linked to a data record, and requires human validation and re-entry each time

AI extracts logic model from uploaded investment memos and auto-populates fields in the entity record — no manual re-entry; linked to the portfolio company's persistent ID

CSDDD Evidence Chain

No native audit trail — assessments, corrective actions, and re-surveys exist in separate sessions with no documented entity linkage; cannot satisfy effectiveness proof requirement

Full timestamped chain: initial assessment → corrective action plan (linked to entity) → follow-up assessment → theme frequency comparison — formatted for regulatory submission

Portfolio Scaling

Each new company or supplier requires manual file preparation, prompt design, and output review — scales linearly with analyst hours

Rubric and data model configured once; AI scoring activates for every new submission automatically — portfolio grows from 20 to 40+ companies without proportional headcount increase

Financial Doc Parsing

Can extract metrics from an uploaded PDF — but output is not stored, not linked to an entity record, and must be re-run and manually entered each reporting cycle

Financial documents uploaded to entity record; key metrics auto-extracted and populated into portfolio fields — stored, linked, and comparable across all reporting cycles

What Sopact Sense produces — ESG due diligence deliverables

Portfolio DDQ scorecard: all entities ranked by composite E, S, G score with pillar breakdown traced to source responses

AI thematic analysis report: theme frequency by rubric category across all entities — forced labor, retaliation, governance gaps, gender leadership

Logic model library: AI-extracted theory of change for each portfolio company or investee, stored in their persistent entity record

Financial metrics dashboard: key indicators auto-extracted from uploaded documents, comparable across the full portfolio

Corrective action tracker: each flagged entity's remediation plan linked to their record, with follow-up assessment data connected automatically

Sopact Sense structures data at the point of collection — so AI analysis is consistent, entity tracking is automatic, and your CSDDD evidence chain is built from day one.

Step 5: ESG Due Diligence Monitoring and CSDDD Effectiveness Proof

After the first assessment cycle, the question shifts from "what does this entity score?" to "is the situation improving, and can we prove it?" This is where the Scoring Trap becomes most dangerous — and where Sopact Sense's persistent ID architecture delivers its clearest differentiator over static compliance tools.

CSDDD does not require that you conducted due diligence. It requires that you can prove your due diligence was effective at preventing harm. Static audit scores refreshed annually cannot satisfy that requirement. What satisfies it is a connected evidence chain: initial assessment → corrective action plan linked to that entity's record → follow-up worker survey on the same entity → score change on the specific dimensions where action was taken → AI analysis showing whether the qualitative themes that generated the corrective action actually decreased in frequency.

For an impact fund with 40 portfolio companies, this means quarterly portfolio updates where each company's current metrics are compared against prior cycles without manual data reconciliation. Dashboards generated in minutes. The fund manager who told their analyst to spend 80% of their time cleaning data gets that time back for analysis.

For development finance institutions monitoring 3–5 year investment periods, this means the gender-smart indicators tracked at application — women in leadership percentage, gender-disaggregated beneficiary outcomes — automatically connect to the same investee's progress reports every six months through the persistent ID chain. Re-scoring from scratch each year is the Scoring Trap. Building on the longitudinal record is the contextual intelligence destination.

For supply chain compliance, this is the CSDDD effectiveness proof in its most concrete form: Supplier X was flagged for forced overtime themes in Q1 worker surveys. A corrective action was documented and linked to Supplier X's persistent record in Sopact Sense. Q3 worker surveys on the same supplier population show "forced overtime" theme frequency dropped from 34% to 8% of responses at that site. That evidence chain — collection, corrective action, re-collection, comparison on the same entity — is only possible when all data is collected inside the same platform, linked to the same entity ID from the beginning.

Watch

Why Data Lifecycle Architecture Determines ESG Due Diligence Quality

How the Data Lifecycle Gap — collecting data in one system and analyzing it in another — is the structural cause of the 80% cleanup tax in ESG due diligence workflows.

ESG due diligence is the structured assessment of an organization's environmental, social, and governance practices — evaluating climate risk, labor standards, board governance, and stakeholder engagement to identify risks that financial analysis alone misses. It applies to pre-investment screening, ongoing portfolio monitoring, supplier evaluation, and grant assessment.

What is an ESG due diligence checklist?

An ESG due diligence checklist covers three pillars: Environmental (emissions, climate risk, resource management, compliance), Social (labor practices, human rights, DEI, stakeholder engagement), and Governance (board structure, executive accountability, ethics, reporting). A functional checklist is a structured data collection instrument designed for AI analysis from submission — not a static PDF checklist.

What is ESG due diligence meaning in practice?

In practice, ESG due diligence means designing structured instruments that capture qualitative and quantitative data from the same entity, assigning persistent IDs so every assessment cycle connects automatically, and using AI to analyze open-ended responses alongside scored metrics. The output is an evidence-linked report — not a point-in-time score — that supports longitudinal effectiveness documentation.

What is an ESG DDQ?

An ESG due diligence questionnaire captures structured quantitative metrics, scored qualitative dimensions, and open-ended narrative responses simultaneously. Effective DDQs are designed inside the platform that will analyze them — so every field is immediately analysis-ready without manual export and reformatting.

What is The Scoring Trap in ESG due diligence?

The Scoring Trap is the pattern where ESG due diligence optimizes for auditable scores rather than actual understanding. ESG scores for the same entity vary up to 50% across providers, reflect self-reported compliance rather than stakeholder reality, and cannot satisfy CSDDD's requirement to prove due diligence effectiveness over time. Sopact Sense enables a progression from SROI-style scoring as an entry point to contextual intelligence as relationships deepen.

What is the ESG due diligence framework?

An ESG due diligence framework governs how assessments are structured, scored, and connected over time. A modern framework covers four stages: (1) Entity intake and DDQ with persistent ID assignment at first contact, (2) AI scoring and thematic analysis of qualitative and quantitative responses, (3) Report generation with score traced to source evidence, (4) Longitudinal monitoring linking each cycle's data to the same entity record.

What is ESG due diligence methodology?

ESG due diligence methodology covers how environmental, social, and governance factors are identified, weighted, assessed, and documented. Modern methodology distinguishes between scoring-based approaches (appropriate for early-stage screening) and contextual intelligence approaches (appropriate for ongoing monitoring) — recognizing that scores alone cannot satisfy CSDDD's "prove effectiveness" standard.

What tools are best for AI ESG due diligence?

Generic AI tools like ChatGPT and Gemini are useful for drafting but structurally unreliable for portfolio-scale ESG due diligence — they produce non-reproducible analysis, lack persistent entity memory, and create disaggregation inconsistencies across sessions. Purpose-built platforms that design data collection inside the analysis environment, assign persistent IDs at first contact, and analyze qualitative and quantitative data in the same system are appropriate for fund-level and compliance-level due diligence.

What is ESG vendor due diligence?

ESG vendor due diligence assesses suppliers and vendors against environmental compliance, labor standards, and governance criteria using structured DDQs, worker voice surveys, and audit data — all designed and collected inside the same platform. Effective vendor due diligence connects each vendor's initial assessment to corrective action plans and follow-up surveys through persistent entity IDs, enabling CSDDD longitudinal effectiveness tracking.

How does ESG due diligence work for impact investors?

For impact investors, ESG due diligence assesses portfolio companies on theory of change clarity, social and environmental impact potential, financial sustainability, and governance quality — at pre-investment and quarterly during the portfolio period. Sopact Sense extracts logic models from investment memos automatically, parses financial documents into portfolio records, and connects each assessment cycle through persistent entity IDs without analyst-intensive reconciliation.

What is the difference between ESG due diligence and ESG reporting?

ESG due diligence is the assessment process — collecting, scoring, and analyzing data to inform a decision. ESG reporting is the output process — presenting performance data to funders, regulators, and stakeholders. Sopact Sense supports both: the same data collected during due diligence generates the nonprofit impact reports and donor impact reports required afterward, without duplicate data entry.

How do I build an ESG due diligence report?

An effective ESG due diligence report includes entity scores by pillar traced to source responses, AI thematic coding of qualitative narratives, financial metrics extracted from uploaded documents, flagged discrepancies between qualitative and quantitative data, and longitudinal comparison to prior cycles. Sopact Sense generates this from data collected inside the platform — no manual assembly from exported spreadsheets across multiple tools.

📁

For Impact Funds & ESG Portfolios

Stop reopening DD folders the week before your LP call.

Every investee story is buried in 50–200 documents that were never designed to connect to each other. Sopact reads them all, carries every DD commitment forward, and generates six LP-ready reports overnight — so your team stops rebuilding context from scratch every quarter.